By the 19th century, a “Common Sense” movement had arisen in America, wherein practical reason and everyday common sense sufficed to understand the world. Whatever its merits, common sense is certainly in short supply in the markets nowadays. A quip by a corporate or civic authority or a market “expert,” and “investors” are off to the races and on rarer occasions, heading for the exits.

The precious metal market has defied common sense for many months. Beyond fundamentals, this market, especially silver, has behaved in the classic pattern of a manic market top. Silver prices increased, usually on the upside, by two to three percent daily in the last months of 2025 and even greater in the last month. For this reason, the CME thrice raised its margin requirements in the last month. Moreover, the closing daily price of silver rose from around $70 USD per ounce in the beginning of January to $115 USD just two days ago.

Grady, you don’t have special powers. You don’t have the ability to look at a guy and “just know” because you’re a scout with special powers. I’ve watched you sit at kitchen tables for years and tell the parents of a 17 year old kid, “Trust me, when I know, I know, and when it comes to your son, I know” and you don’t.

– Moneyball (2011)

Scornful mirth arises when, on the eve of a crash, “experts” at big financial institutions, such as the Bank of Montreal or the Bank of America or Joseph Cavatoni, senior market strategist at the World Gold Council (WGC), promise the sky’s the limit. Not all institutional and self-anointed experts engage in shill boosterism.

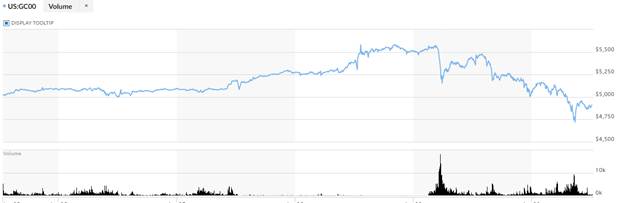

It is especially irksome when the representative from the WGC promotes these claims on the very day that his organization publishes its annual year-end Gold Demand Trends report. For it was the WGC report on Thursday, not Trump’s choice of Fed Chairman on Friday which provoked the crash in gold (8.5%) and silver market (25.5%) markets. These were down as much as 12% and 33% respectively.

However, it was on Thursday morning, when the WGC released its report, that the gold and silver market fever broke. At 1:00 am (EST), when Reuters reported on the WGC release, February gold futures were over $5,600/oz. By 10:40 am, futures had plummeted to $5,100, a drop of 9%, before the ‘buy the dip’ momentum crowd restored the price to just shy of $5,500 by 7:40 pm. The price thereafter dropped to $4,700 by 1:30 pm on the following day before recovering to $4,909/oz.

The Pin Prick Trigger

The WGC report revealed that gold demand plummeted for end users, for jewelry by 19% year-over-year, and central bank and institutional accumulation by 37%. The slack was taken up by “investors,” who nearly doubled their purchases.

We in the GTA area observed this pattern recently in the Toronto condo market. During the FOMO mania, sales of condos, many on spec, climbed through the roof. Many condos were mere shoeboxes, perhaps livable as university residences, more useful as high-priced hookers’ lairs. Investors were pumping up condo prices among themselves, hoping to sell before they had to take possession. Inevitably, Wiley E. Coyote eventually found no terra firma under its feet.

If the real gold market was finding far fewer end users, this would be more so for the real silver market. Even the mid-year Interim Market Review by the Silver Institute had predicted that industrial use of silver in 2025 likely declined by 4% from 2024, 3.5% below earlier estimates that year. Decline was partly due to technological proficiencies (re: “progressive thrifting,” some substitution with copper). Another report expects “silver jewelry and silverware demand to decline by 4% and 11%, respectively.” But these prognostications were prior to recent price spikes in silver.

Economics 101 insists upon an inverse relationship between price and demand. While the silver market was entering its sixth year of supply deficit, extraordinary price spikes have an irritating habit of briskly reversing that trend as in the early 1980s.

Moreover, the gold to silver price ratio had declined from 104x (April 2025) to 46x on Thursday. The recent historical average is 68x. Just as excessively high ratios suggest a faster runup in silver prices in 2025, a corresponding excessive low ratio suggest a much greater reversal for silver in 2026.

A Little Gully

The shills are already out in force suggesting that yesterday’s crash was merely a typical and much needed correction. Something structural has changed according to them. (“And once something is anchored, the discussion changes.”) It is different this time.

“Buy the dip” momentum speculators will likely see this crash as opportunity, as their “ancestors” so thought in early 1930. A day trader might be wise to anticipate extreme volatility in the days to come, rather than heavily shorting the price of silver. There shall be many margin calls. With present margin requirements at 9%, many dealers will be hurt and demand higher margin rates going forward. This may instigate further prices declines.

Nevertheless, silver prices shall eventually decline to market equilibrium, if not below. If demand for gold by central bankers, financial institutions, and end users was precipitously dropping when the price of gold was $4,135/oz, how much more so when the price is $4,900/oz? If the price for silver has tripled in under one year, how sustainable is end-user demand?

Despite claims by shills, silver is not legal tender. It is not a currency and cannot be so if daily prices rise and fall by several percentage. The same is true of crypto currencies. The whole telos of currency is to provide financial and economic stability. If the complaint against 1970s style inflation was unpredictability, leading to less business investment, how much more so for a wildly fluctuating “currency?”

With supply deficit constraints, silver cannot be accumulated in bulk as a reserve. If countries are now accumulating silver, it is for the critical purpose of secure industrial supply. While there is a long-term business case for increased demand for silver, much higher prices incentivize technological proficiencies and open mothballed silver mines. There are reasonable economic limits to the price of silver. Anything above that limit is a plaything for the rentiers at the expense of the producers.